Global equity markets remain buoyant as US stocks reach an all-time high

Global equity markets remain buoyant as US stocks reach an all-time high

07 Feb 2024

Month in brief

- Global equities built on their convincing finish to 2023 driven by strong performance from US stocks.

- However, emerging market equities suffered losses as the Chinese regulator stepped up its efforts to subdue a stock market freefall.

- As expected, the Bank of England and the Federal Reserve both voted to leave interest rates unchanged.

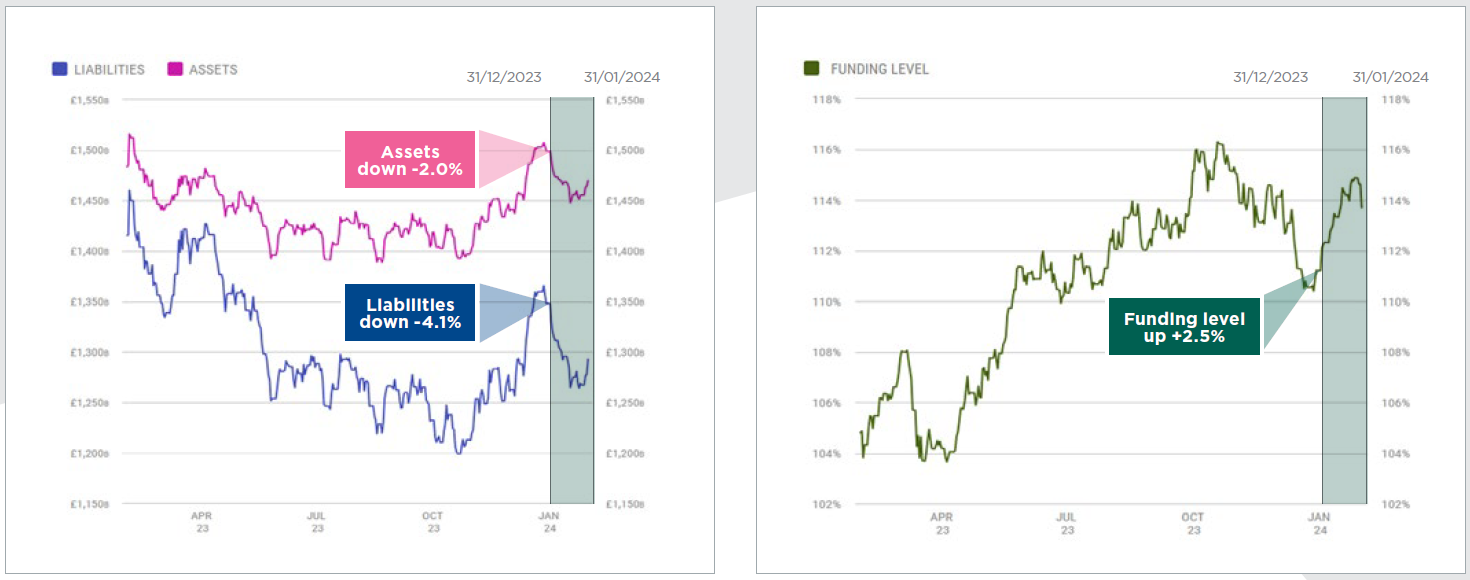

- DB pension scheme funding on a low-risk basis rose sharply over the month thanks to rising gilt yields.

January saw the FTSE All-World Index deliver its third consecutive month of strong growth largely thanks to US stocks which benefitted from a technology rally after a more subdued start to the month.

US equities – which account for around 60% of the global stock market – reached a new peak during January and propelled global equities overall to build on their formidable momentum from the fourth quarter of 2023. However, regional performance around the globe was inconsistent and UK equities were unable to reach positive territory despite a rally in the second half of the month.

Emerging market equities performed particularly poorly as almost all of December’s gains were wiped out as China continued to underperform. The Chinese Securities Regulatory Commission has come under increasing pressure to try and stem a prolonged sell-off and it introduced official measures in January to restrict the short selling of Chinese stocks after attempted informal measures failed. Investor confidence in China’s growth prospects has been waning for some time and a further blow was dealt in January when indebted property giant Evergrande was formally ordered into liquidation.

UK corporate bonds delivered negative performance despite a modest tightening in credit spreads. High-yield bonds ended the month up thanks to more encouraging data suggesting that inflation, especially in the US, was continuing to move in the right direction and borrowing costs would begin to come down soon. Interest rates in the US were held constant in January but markets are pricing in a strong possibility that the Federal Reserve will vote to reduce rates at its March meeting.

UK interest rates were held at 5.25% in early February and the UK Consumer Prices Index now stands at 4.0% compared to its peak of 11.1% in October 2022. The Bank of England cautioned that more evidence is needed to demonstrate that inflation will continue to fall before interest rate cuts would be seriously considered. However, for the first time since 2020, a member of the Monetary Policy Committee voted for a cut in interest rates at the February meeting.

During January long-term gilt yields rose sharply as investors curbed their optimism over the potential for significant interest rate cuts in the UK over 2024. This resulted in fixed interest and index-linked gilts performing poorly and the recent volatility in gilt markets is expected to persist as the pace at which interest rates may start to come down remains uncertain.

Aggregate UK DB pension scheme funding on a low-risk basis rose over the month as rising gilt yields reduced liabilities by more than assets. The sharp improvement in funding over January largely offset the deterioration seen over the fourth quarter of 2023.

Source: XPS DB:UK www.xpsgroup.com/services/xps-pensions/xps-dbuk-funding-watch

The charts above are based on data from The Pensions Regulator, the PPF 7800 Index and the XPS data pool. The assumptions used in the UK:DB long-term target basis include a discount interest rate of gilt yields plus 0.5%. The assumed asset allocation is 16.9% equities, 20.0% corporate bonds, 6.9% multi-asset, 5.1% property, 3.8% private markets and 47.3% in liability-driven investment (LDI) with the LDI overlay providing a 60% hedge on inflation and interest rates.

For further information, please get in touch with James Kidd or your usual XPS contact.